Medical Travel Insurance for Pre-Existing Conditions: The 2026 Complete Guide

- Apr 30

- 12 min read

What if a minor medication adjustment made 89 days ago is the specific reason a carrier denies your $50,000 emergency claim? You likely understand that traveling with a chronic illness requires extra preparation; it's stressful to worry that a look-back period might leave you stranded in a foreign hospital without financial support. Securing reliable medical travel insurance for pre-existing conditions shouldn't feel like a clinical gamble. You deserve to know that your policy is as stable as your health before you ever reach the airport gate.

This 2026 guide simplifies the complexities of look-back windows and clinical waivers to ensure your next journey is protected both financially and medically. We'll outline the specific clinical requirements for safe flight and explain how to verify your coverage is active before an emergency occurs. You'll learn the exact steps to secure a pre-existing condition waiver, providing the peace of mind your family needs for a stress-free experience. Our goal is to ensure you feel supported by a steady hand throughout your entire trip.

Key Takeaways

Understand how the 2026 look-back period affects your eligibility and what specific medical history insurers scrutinize to ensure your coverage remains uncompromising.

Learn the essential steps to secure a waiver within the critical purchase window, ensuring your medical travel insurance for pre-existing conditions provides the comprehensive protection you need.

Identify the critical gap between standard financial insurance payouts and the specialized clinical safety required for a seamless medical repatriation.

Access a professional safety checklist to verify your policy's written coverage and manage your medication supply with the precision required for international travel.

Discover how bedside-to-bedside coordination by a professional flight nurse preserves patient dignity and provides peace of mind during high-stress medical transfers.

Table of Contents Understanding Pre-Existing Conditions and the Look-Back Period How to Secure a Pre-Existing Condition Waiver in 2026 Financial Coverage vs. Clinical Safety: The Gap in Standard Insurance A Safety Checklist for Travelers with Chronic Illness RN MEDflights: Professional Escorts for Travelers with Pre-Existing Conditions

Understanding Pre-Existing Conditions and the Look-Back Period

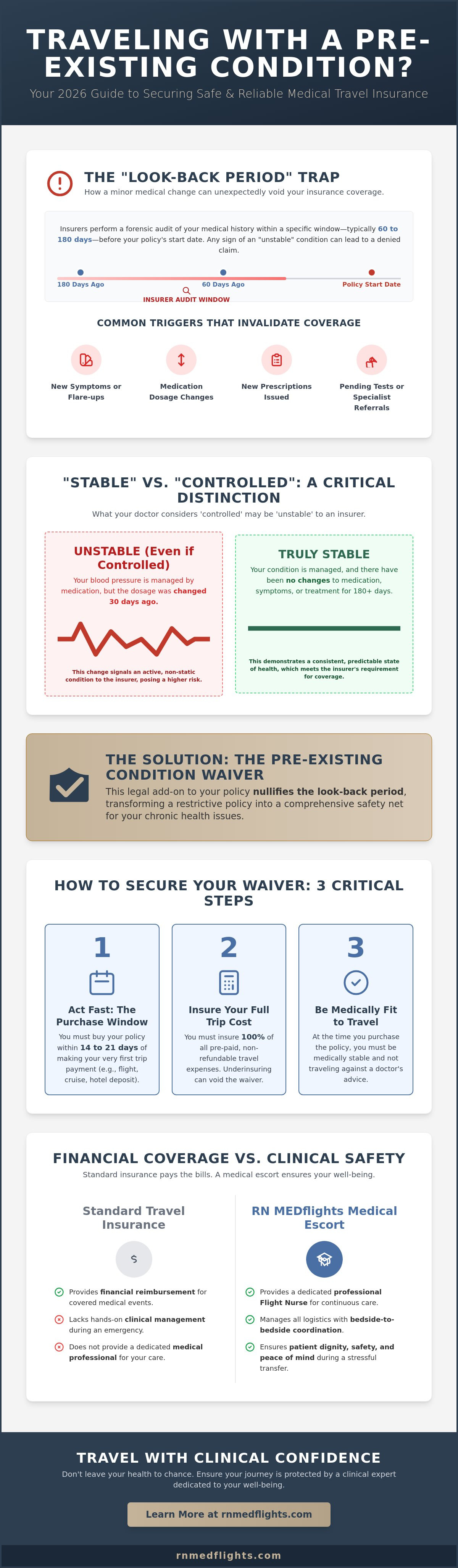

In the 2026 travel environment, securing medical travel insurance for pre-existing conditions starts with a clear grasp of clinical insurance terminology. Providers define these conditions as any health issue for which you sought medical advice, received treatment, or experienced symptoms before your policy's effective date. For a foundational perspective, Understanding Pre-Existing Conditions helps clarify how these definitions apply across the global insurance industry. The insurer's primary focus is not just your diagnosis, but the clinical stability of your health during a specific timeframe known as the look-back period.

This look-back period typically spans 60 to 180 days. It serves as a window for insurers to audit your medical history once a claim is filed. If you experienced new symptoms or underwent diagnostic tests 45 days before your departure, the insurer may deem your condition unstable. Even a minor change in prescription dosage can reset your stability clock. Whether your physician increased a dose to manage symptoms or decreased it because you're improving, the insurance company views any adjustment as a sign that the condition is not in a steady state. This rigid clinical standard ensures that only truly stable patients are covered under standard terms, prioritizing the safety of the traveler and the liability of the provider.

What Qualifies as a Condition?

Chronic illnesses like COPD, congestive heart failure, and Type 2 diabetes are the most common conditions requiring disclosure. However, the definition extends to any recent surgeries or treatments currently under follow-up care. For example, a cardiac procedure performed 120 days ago is still a pre-existing condition if you're attending rehabilitation sessions. Mental health conditions and dementia are also scrutinized. Insurers view these as significant risks during travel due to the potential for acute episodes or disorientation in unfamiliar environments, requiring specialized documentation for coverage.

The Look-Back Period Explained

Providers conduct a forensic review of your medical records after an incident occurs. Common triggers that invalidate coverage include a doctor’s recommendation for a specialist consultation you haven't attended yet or a new prescription for a recurring symptom. You must distinguish between "stable" and "controlled" status. You might have your blood pressure controlled with medication, but if that medication changed 30 days ago, you aren't considered stable in the eyes of an underwriter. This distinction is critical when seeking medical travel insurance for pre-existing conditions, as it dictates whether a claim for an emergency evacuation or hospital stay will be honored or denied based on the medical timeline.

How to Secure a Pre-Existing Condition Waiver in 2026

Securing a waiver is the most reliable method to ensure your policy covers chronic health issues. This legal addition to your plan nullifies the standard look-back period, which typically spans 60 to 180 days before your purchase date. Without this waiver, insurers will scrutinize your medical records for any changes in medication, new symptoms, or diagnostic tests during that window. For travelers managing long-term health challenges, this document transforms a restrictive policy into a comprehensive safety net.

The 14-Day Rule: Timing is Everything

Timing dictates your eligibility for medical travel insurance for pre-existing conditions. Most carriers in 2026 require you to purchase your policy within 14 to 21 days of making your initial trip deposit. This first deposit includes any payment made toward airfare, cruises, or hotel stays. If you miss this window, you likely lose the opportunity to secure a waiver for that specific journey. For multi-leg journeys or complex cruise bookings, the clock starts the moment you pay for the first segment.

You should consult a guide to travel insurance for pre-existing conditions to understand how different providers define these strict deadlines. You must also insure 100% of your non-refundable costs. If you underestimate your trip value or fail to update the policy when adding new excursions, the insurer may void the waiver during the claims process. Accuracy in your financial reporting is just as vital as accuracy in your medical history.

Proving Medical Stability

You must be medically fit to travel on the day you buy your policy. This requirement doesn't mean you must be cured; it means your condition is stable. We recommend requesting a formal letter of stability from your primary care physician or specialist before booking your trip. This document should confirm that no treatment changes, new prescriptions, or diagnostic tests are pending.

Insurance adjusters use specific ICD-10 diagnostic codes to evaluate claims. Having your physician document your status clearly helps avoid disputes if you require a medical evacuation. For patients in remission or those with asymptomatic conditions, this documentation provides a vital paper trail. Our flight coordinators often see how detailed medical records simplify the transition to specialized care if a crisis occurs. To maintain the integrity of your claim, keep a dedicated folder containing:

A current list of all medications and dosages.

Recent lab results or imaging reports.

A signed statement of "fitness for travel" from your specialist.

Receipts for every non-refundable trip expense.

This proactive approach ensures that your focus remains on your recovery rather than administrative hurdles. Our nurse-led team remains available 24/7/365 to provide the clinical support and bedside-to-bedside care that families rely on during high-stress transitions.

Financial Coverage vs. Clinical Safety: The Gap in Standard Insurance

A common misconception exists that a valid policy for medical travel insurance for pre-existing conditions ensures a seamless trip home after a health crisis. In reality, a financial payout is not a logistical solution. Insurance companies focus on "medical necessity," which often means they only cover transport if local facilities cannot provide life-saving care. If a hospital in a foreign country can stabilize a chronic condition, the insurer may deny a claim for repatriation. This leaves the patient to manage their own travel while still medically fragile, prioritizing the insurer's bottom line over the patient's long-term recovery.

Airlines maintain the ultimate authority to refuse boarding to any passenger they deem unstable or a safety risk. Even with a paid insurance claim, a patient might be turned away at the gate if they require continuous oxygen or specialized monitoring. This is where medical escort services bridge the gap. These professionals provide the clinical oversight required to satisfy airline safety standards while ensuring the patient’s health doesn't deteriorate during the journey. We act as a steady hand, managing the complex intersection of aviation rules and clinical requirements.

Insurance Exclusions You Need to Know

Standard policies frequently exclude the cost of a medical escort on commercial flights, viewing it as a luxury rather than a requirement. While you can find official information on pre-existing conditions regarding domestic coverage protections, travel policies operate under different mandates. Many travelers don't realize that "medical evacuation" often only covers transport to the nearest adequate facility. This might be a hospital three countries away from your home. True bedside-to-bedside care is rarely a default feature; it requires specialized coordination that standard insurers aren't equipped to handle 24/7/365.

The 'Fit to Fly' Hurdle

Securing an airline’s medical clearance involves the rigorous Medical Information Form (MEDIF) process. A simple doctor’s note isn't sufficient for patients with chronic respiratory or cardiac issues. Airlines evaluate the risk of in-flight emergencies, often requiring technical data on oxygen flow rates or mobility limitations before granting access to the cabin. Our flight nurses manage these risks by providing advanced life support capabilities within the commercial environment. They act as a clinical advocate, translating complex medical data into the safety language airlines require. This specialized intervention ensures that medical travel insurance for pre-existing conditions actually results in a successful journey home rather than a denied boarding at the airport.

A Safety Checklist for Travelers with Chronic Illness

Preparing for international travel with a chronic condition requires more than just packing a suitcase. It demands a clinical level of organization to ensure your safety and the validity of your coverage. Before you depart, verify your policy explicitly includes a pre-existing condition waiver in writing. Verbal assurances from a broker won't suffice during a claim. This document is your primary defense when utilizing medical travel insurance for pre-existing conditions.

A rigorous preparation process includes the following steps:

Secure a written waiver: Ensure the insurance carrier has acknowledged your specific medical history and waived the standard look-back period.

Pharmacy verification: Carry a 30-day supply of all medications in their original pharmacy packaging. This prevents customs delays and ensures foreign clinicians can identify your exact dosages.

Clinical documentation: Obtain a comprehensive medical summary from your treating physician. This should include your current ICD-10 codes, recent lab results, and a list of contraindicated treatments.

Repatriation planning: Pre-arrange international medical repatriation services for high-risk relocations to ensure a seamless transition back to your home hospital if a crisis occurs.

Infrastructure audit: Research the local medical facilities at your destination. Confirm they have the specialized equipment, such as dialysis units or cardiac catheterization labs, required for your care.

Medication and Equipment Logistics

If you use a portable oxygen concentrator (POC), confirm it's FAA-approved and bring enough battery life for 150% of your total flight time. This extra capacity accounts for unexpected tarmac delays or diverted flights. For those managing temperature-sensitive medications like insulin, use a dedicated medical cooling case with a built-in thermometer. Don't rely on hotel mini-fridges, as they often lack consistent temperature control. Always carry a physical backup prescription. Foreign pharmacies might not accept your digital records, but a signed paper script from your doctor provides a clear path to an emergency replacement.

Emergency Contact and Data Management

Set up a digital medical ID on your smartphone that's accessible from the lock screen. This allows first responders to see your blood type, allergies, and emergency contacts instantly. Share your full itinerary and clinical needs with a dedicated flight coordinator. Having a professional advocate who understands your medical history significantly reduces response times during a crisis. Finally, identify 'Centers of Excellence' near your destination. These are specialized facilities that meet international standards for conditions like cardiac care or oncology. Knowing exactly where to go before an emergency happens provides the peace of mind necessary for a stress-free journey.

For professional bedside-to-bedside support and expert medical logistics, contact the specialists at RN Medflights.

RN MEDflights: Professional Escorts for Travelers with Pre-Existing Conditions

Travelers managing chronic illnesses often find that even the most comprehensive medical travel insurance for pre-existing conditions leaves a logistical gap in actual physical care during transit. RN MEDflights fills this void by providing specialized medical escorts for commercial flights. This service offers a cost-effective alternative to private air ambulances, which often cost between $25,000 and $100,000 depending on the distance. By utilizing commercial airlines, we provide a solution that is both financially accessible and clinically rigorous.

The role of a flight nurse involves much more than companionship. At 35,000 feet, physiological changes like decreased barometric pressure can exacerbate respiratory or cardiac issues. Our nurses are trained to recognize these shifts before they become emergencies. They bring the expertise of an intensive care unit to a standard airline seat, ensuring every patient reaches their destination in stable condition. We manage the medical complexities so that your insurance coverage focuses on the financial side while we focus on the human side.

Why a Nurse-Led Approach Matters

Clinical precision is the foundation of our service. For patients with dementia, the stress of travel often triggers agitation or confusion. Our nurses utilize specialized communication techniques to maintain the patient's dignity and calm throughout the journey. For those with cardiac or respiratory needs, we provide continuous vital sign monitoring and precise medication administration. We don't just react to problems; we prevent them through proactive symptom assessment. This nurse-centric model provides the emotional peace of mind families need during a stressful relocation. We treat every traveler as a person, not a case number.

Coordinating Your Journey Home

Our team handles every logistical detail to ensure a seamless experience. We navigate the complex medical desks of global airlines to secure clearances and appropriate seating. The RN MEDflights commitment to bedside-to-bedside care means we manage the entire chain of responsibility. Our coordination includes:

Securing ground ambulance transfers from the originating hospital to the airport terminal.

Managing all luggage and medical equipment through security and customs checkpoints.

Arranging for ground transport at the arrival city directly to the receiving facility or private residence.

Our flight coordinators are available 24/7/365 to respond to global medical repatriation needs. We act as a steady hand in the storm, managing the hurdles so you can focus on recovery. By integrating medical expertise with logistical mastery, we ensure that having a pre-existing condition doesn't mean you have to stay grounded. We provide the specialized care necessary to bridge the gap between a medical crisis and a safe return home.

Securing Your Health and Mobility for 2026 Travels

Navigating medical travel insurance for pre-existing conditions in 2026 requires precise attention to the standard 60 to 180 day look-back period and the strict 14 to 21 day window for securing a waiver. While insurance provides a financial safety net, it doesn't offer the clinical hands-on care required during a mid-air crisis. You need a solution that bridges the gap between a policy payout and actual medical safety. RN MEDflights provides this essential layer of protection through our veteran-owned and nurse-led expertise.

Our team specializes in seamless bedside-to-bedside international repatriation, ensuring you're never left alone during complex transitions. We offer cost-effective commercial flight stretcher options that maintain uncompromising clinical standards. It's about more than just logistics; it's about providing the dignity and specialized care you deserve. Whether you're managing a chronic illness or recovering from surgery, our flight coordinators are available 24/7/365 to manage every detail of your journey. You can reclaim your freedom to explore the world while knowing professional help is always within reach.

Take the first step toward a safe and stress-free journey today. Request a Quote for Professional Medical Escort Services and let our medical experts handle the rest. Your health is our mission, and we're ready to bring you home safely.

Frequently Asked Questions

Does travel insurance cover pre-existing conditions if I buy it today?

Standard travel policies cover pre-existing conditions only if the condition is stable for a specific period, typically 60 to 180 days. If your health changed or you adjusted medications within this window, the insurer excludes that condition. You'll need a specific waiver to ensure full protection. Our team at RN Medflights is available 24/7/365 to help you navigate these clinical requirements before you book your transport. This ensures your medical needs are met with uncompromising integrity.

What is a pre-existing condition waiver and how do I get one?

A pre-existing condition waiver is a policy add-on that prevents the insurer from investigating your medical history during a claim. To qualify, you must purchase medical travel insurance for pre-existing conditions within 14 to 21 days of making your initial trip payment. You must also be medically fit to travel on the day you buy the policy. This document provides the essential safety net for patients with chronic illnesses.

Can I fly with a heart condition or COPD if I have insurance?

You can fly with these conditions if a doctor confirms you're fit for flight and your symptoms haven't changed in the last 90 days. Heart conditions and COPD require careful monitoring because cabin altitudes reach 8,000 feet, which reduces available oxygen. RN Medflights specializes in these high-risk transfers. Our flight coordinators arrange specialized equipment like portable oxygen concentrators to maintain your safety throughout the journey.

Will insurance pay for a medical escort to fly home with me?

Most comprehensive policies pay for a medical escort if a doctor certifies that you require clinical supervision to return home. This benefit falls under the emergency medical evacuation coverage. Our registered nurses provide bedside-to-bedside care, managing medications and monitoring vitals during the flight. It's a seamless process that prioritizes your dignity and health during a stressful transition. We handle every logistical detail to ensure a stress-free experience.

How far back do travel insurance companies look into my medical history?

Insurance companies typically examine the 60 to 180 days of your medical records immediately preceding your policy purchase. This timeframe is known as the look-back period. They look for new symptoms, hospitalizations, or any changes in your prescription dosages. If your condition was managed and unchanged during these 6 months, it's usually considered stable for coverage purposes. Our clinical team can help you understand how these timelines affect your transport options.

What happens if I forget to disclose a condition when buying insurance?

Failing to disclose a condition often results in a total claim denial and the cancellation of your benefits. Insurers review 100% of relevant medical records when you file a claim for hospital costs or evacuation. If they find an undisclosed diagnosis from the look-back period, they won't pay for your care. Accuracy is the only way to ensure your peace of mind and financial security. We recommend double-checking all records with your physician.

Is dementia considered a pre-existing condition for travel insurance?

All major insurers classify dementia as a pre-existing condition because it's a chronic, progressive medical diagnosis. Whether your policy covers it depends on if the patient met the stability requirements during the 180-day look-back window. For families dealing with cognitive decline, securing medical travel insurance for pre-existing conditions with a waiver is the most reliable way to guarantee that professional clinical support is available during a crisis. Our nurses prioritize patient dignity during every transport.